Jul 1, 2025

AML (Anti-Money Laundering) Software Development Guide: Build Secure Fintech Apps

Explore AML (Anti-Money Laundering) software development, regulations, and features. Learn how GeekyAnts builds custom AML solutions for fintech apps with AI, compliance, and ROI.

Author

Subject Matter Expert

Book a call

Table of Contents

Key Takeaways:

- AML software must be treated as core financial infrastructure rather than added after launch, as delayed implementation creates monitoring gaps, operational friction, and regulatory exposure.

- An effective AML platform connects customer due diligence, sanctions screening, transaction monitoring, dynamic risk scoring, case management, audit trails, and regulatory reporting within one coordinated workflow.

- Financial products operating across markets need configurable rules, scalable data architecture, and jurisdiction-aware reporting instead of fixed thresholds and disconnected legacy tools.

- AI can improve anomaly detection and alert prioritization, but only when models are explainable, governed, continuously monitored, and supported by human investigation.

Anti-Money Laundering (AML) is no longer just about compliance. Today, it is about protecting the business from the inside out. At its core, AML is the system we design to ensure that illicit money — whether routed through fake accounts, shell companies, or rapid international transfers — does not pass through our platforms unnoticed.

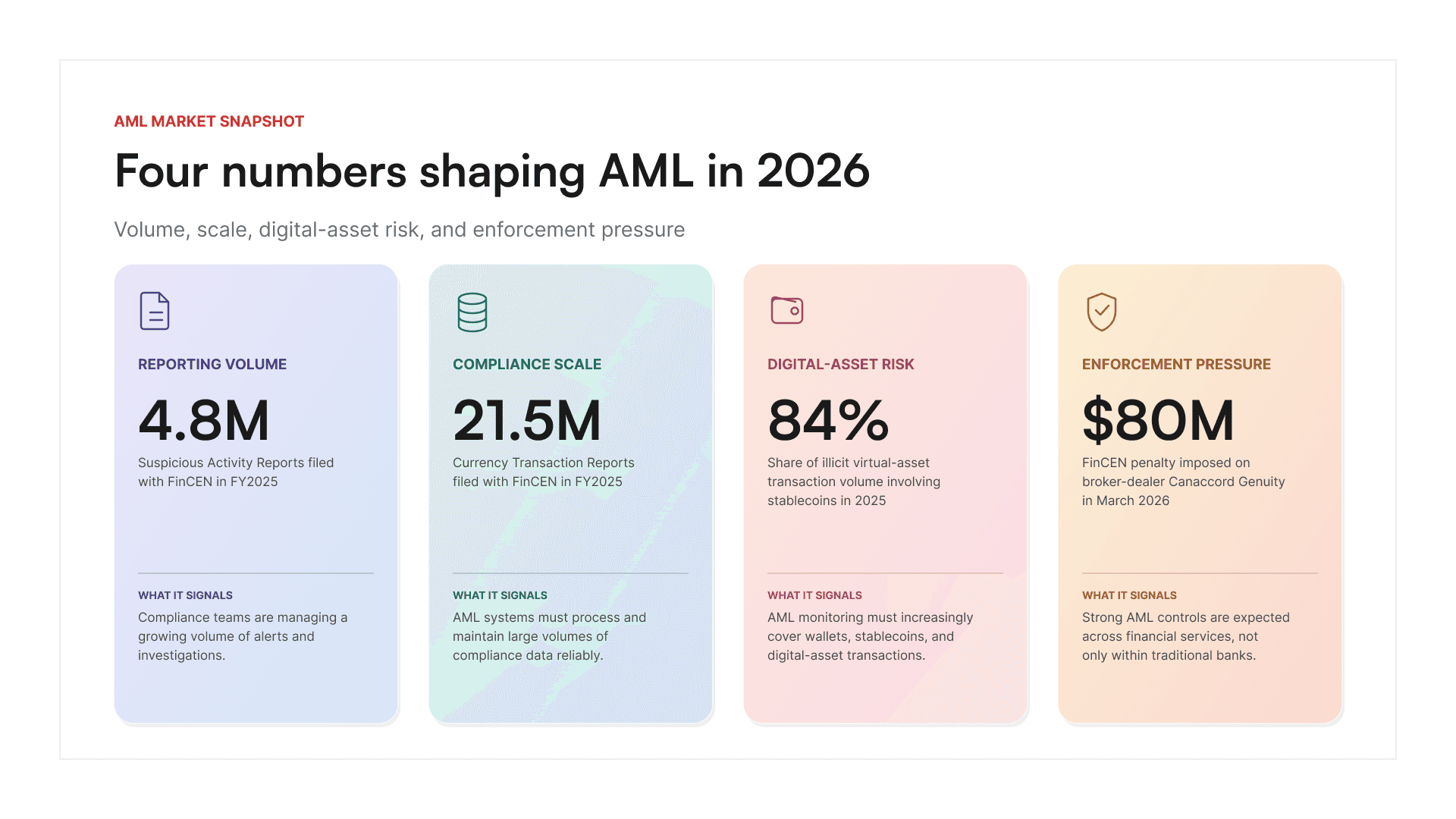

And the pressure is only mounting. According to Fenergo, global regulatory fines for AML, KYC, and sanctions failures jumped 417% compared to the same period a year earlier - driven largely by a crackdown on the crypto sector.

Every dollar moving through your platform is an opportunity for illicit funds to slip in, and today those transactions are faster, more global and more decentralized than ever.

AML is much more than a regulatory checkbox.

What is the cost of non-compliance? Global AML-related fines totalled roughly $3.8 billion in 2025 — following $4.6 billion in 2024 and $6.6 billion in 2023. The headline case remains TD Bank, fined over $3 billion in 2024 after AML failures let drug cartels move illicit funds through its US operations. And enforcement is spreading beyond legacy banks: in 2025, crypto exchange OKX agreed to pay over $500 million, and UK neobank Monzo was fined £21 million for prolonged control failures.

So, if you are building anything in the financial space today — a digital bank, a payment platform, a lending app — AML is not something you can delay or delegate. It must be embedded into the product from day one, as critical as your user experience or core infrastructure.next

Market Overview: What Kind of AML Software Does the Market Demand

If you are still relying on legacy AML infrastructure or cobbling together transaction monitoring as an afterthought, you are sitting on a time bomb. Financial institutions and fintech companies need platforms that can process the ever growing volumes of customers and their transaction data. This includes, recognizing risks across newer payment channels and also maintaining a clear record of complicated transactions.

Overall, these figures reflect a shift in what customers expect from AML technology. The demand has long since moved on from disconnected, reactive tools- towards more integrated platforms that can adapt products, risks, and regulatory expectations change without leaving gaps in monitoring.

“Regulators are no longer tolerating reactive, patchwork AML systems. They expect real-time controls, behavioral risk analysis, and automated escalation that can scale with transaction volumes and regulatory expectations.” - Kunal Kumar, CRO GeekyAnts

What is Anti-Money Laundering or AML Software, and its Various Types

Anti-Money Laundering (AML) software refers to a set of digital tools and systems used to monitor, detect, and report suspicious financial activities that may be linked to money laundering, terrorism financing, fraud, or sanctions evasion. These tools are designed to help financial institutions, fintechs, and other regulated entities comply with global AML regulations such as the Bank Secrecy Act (BSA), FATF guidelines, and the European Union’s AML Directives.

At its core, AML software continuously scans user behavior, transaction patterns, and customer profiles to identify red flags. These can include unusually large transfers, rapid movement of funds across borders, transactions involving high-risk countries, or attempts to bypass know-your-customer (KYC) protocols.

AML software watches. It listens. It waits. It sits quietly behind every transaction, every login, every wire that jumps a border. When something feels wrong—too fast, too big, too clever—it knows. It begins with transaction monitoring to analyze user behavior, payment patterns, and account activity in real time to spot anomalies that may indicate money laundering or fraud.

For example, the system may flag:

- repeated transactions designed to remain below reporting thresholds;

- sudden increases in transaction frequency or value;

- rapid movement of funds between multiple accounts;

- payments involving sanctioned or high-risk entities;

- unusual cross-border transaction patterns; or

- activity inconsistent with a customer’s stated profile.

How Does an AML Software Work

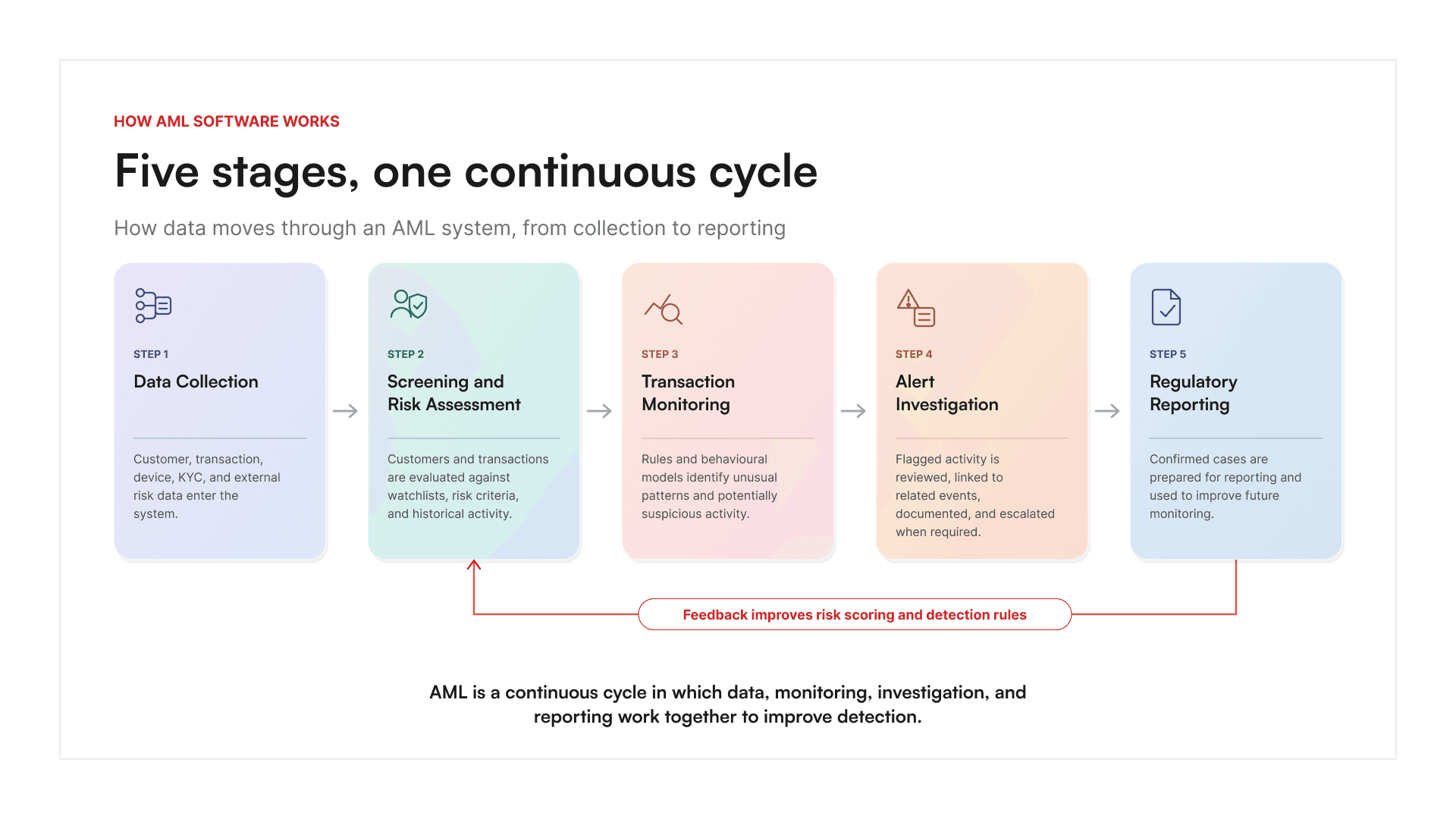

AML software functions through a sequence of modules that work together in near-real time:

1. Data Collection and Consolidation

The system pulls data from various sources: user profiles, KYC documents, transaction logs, third-party sanctions lists (OFAC, UN, etc.), and behavioral signals. It standardises and connects this information so that activity can be accessed across related customers, accounts and transactions.

2. Screening and Risk Assessment

Each user or transaction is screened against global watchlists, politically exposed persons (PEPs), and internal risk policies. A dynamic risk score is assigned based on user behavior, geography, transaction frequency, and historical data.

3. Transaction and Behavioural Monitoring

The system applies pre-configured rules (e.g., daily transaction limits) and machine learning models to detect unusual patterns, such as structuring (smurfing), layering, or circular fund flows.

4. Alerting and Case Management

Suspicious activities trigger alerts, which are routed to compliance teams via case management dashboards. Analysts review the supporting information, connect related alerts, document evidence and record the reasoning behind every decision. Each case is resolved through this investigation workflow.

5. Regulatory Reporting

Confirmed suspicious activity is escalated to the appropriate financial intelligence units (FIUs) through automated Suspicious Activity Reports (SARs), Currency Transaction Reports (CTRs), or equivalent jurisdictional filings. Investigation results can be used to update the customer risk scores, refine detention rules and improve future alert prioritization.

Types of AML Software and Who Uses Them

AML software is not one-size-fits-all. Its design depends on use cases, company size, regulatory scope, and risk exposure. Here are the primary development categories and who uses them:

1. Rule-Based AML Engines

Built on configurable rules and thresholds, these systems work best for small to mid-size financial companies or startups in early compliance phases.

Used by: Digital wallets, neobanks, remittance platforms.

2. AI/ML-Driven AML Systems

These systems use machine learning models to detect patterns and reduce false positives. They improve over time and are ideal for environments with high transaction volumes and user diversity.

Used by: Crypto exchanges, embedded finance providers, enterprise fintechs.

3. Real-Time Transaction Monitoring Platforms

These are optimized for milliseconds-scale processing and in-flight transaction decisions—critical for real-time payment ecosystems.

Used by: Real-time payment apps (like UPI, PIX, RTP), stock trading apps, P2P platforms.

4. Sanctions and Watchlist Screening Modules

Often built as plug-and-play microservices, these modules integrate with onboarding, KYC, or payment APIs to screen users and counterparties.

Used by: SaaS platforms, lending APIs, insurance tech, B2B payment providers.

5. End-to-End AML Compliance Suites

These include all the above, along with case management, audit logs, regulatory reporting, and compliance dashboards.

Used by: Banks, enterprise-grade fintechs, multinational financial service companies

Core Components of AML Software

The core components of AML software work together to create a comprehensive defense against financial crime. Each component serves a distinct purpose—some focus on prevention, others on detection, and many on ensuring regulatory accountability.

From verifying user identities to monitoring millions of transactions in real time, these systems are designed to catch what humans alone might miss.

Here is a list of the core components of AML software in general:

- Customer Due Diligence (CDD) and KYC Integration

Collects and verifies user identity at onboarding, connects with document verification and biometric tools, and maintains ongoing risk assessments. - Transaction Monitoring System (TMS)

Observes and analyzes real-time or batch transactions to detect suspicious behavior such as structuring, rapid movement of funds, or irregular spending patterns. - Sanctions and Watchlist Screening

Cross-references users and entities against global databases such as OFAC, UN, EU sanctions lists, and politically exposed person (PEP) lists. - Risk Scoring Engine

Assigns risk levels to users and transactions based on behavioral, geographic, and historical data, adjusting scores as activity evolves. - Alert Generation and Case Management

Raises alerts for review when thresholds are crossed, providing investigation tools, escalation paths, and audit trails for compliance teams. - Regulatory Reporting Automation

Prepares and submits mandatory reports like Suspicious Activity Reports (SARs) or Currency Transaction Reports (CTRs) to the relevant financial intelligence units (FIUs). - Audit Logs and Compliance Dashboards

Tracks every action taken within the system and provides oversight tools for internal teams and external regulators. - Machine Learning and Advanced Analytics (Optional Layer)

Enhances detection capabilities by learning from historical data, reducing false positives, and surfacing hidden risk patterns.

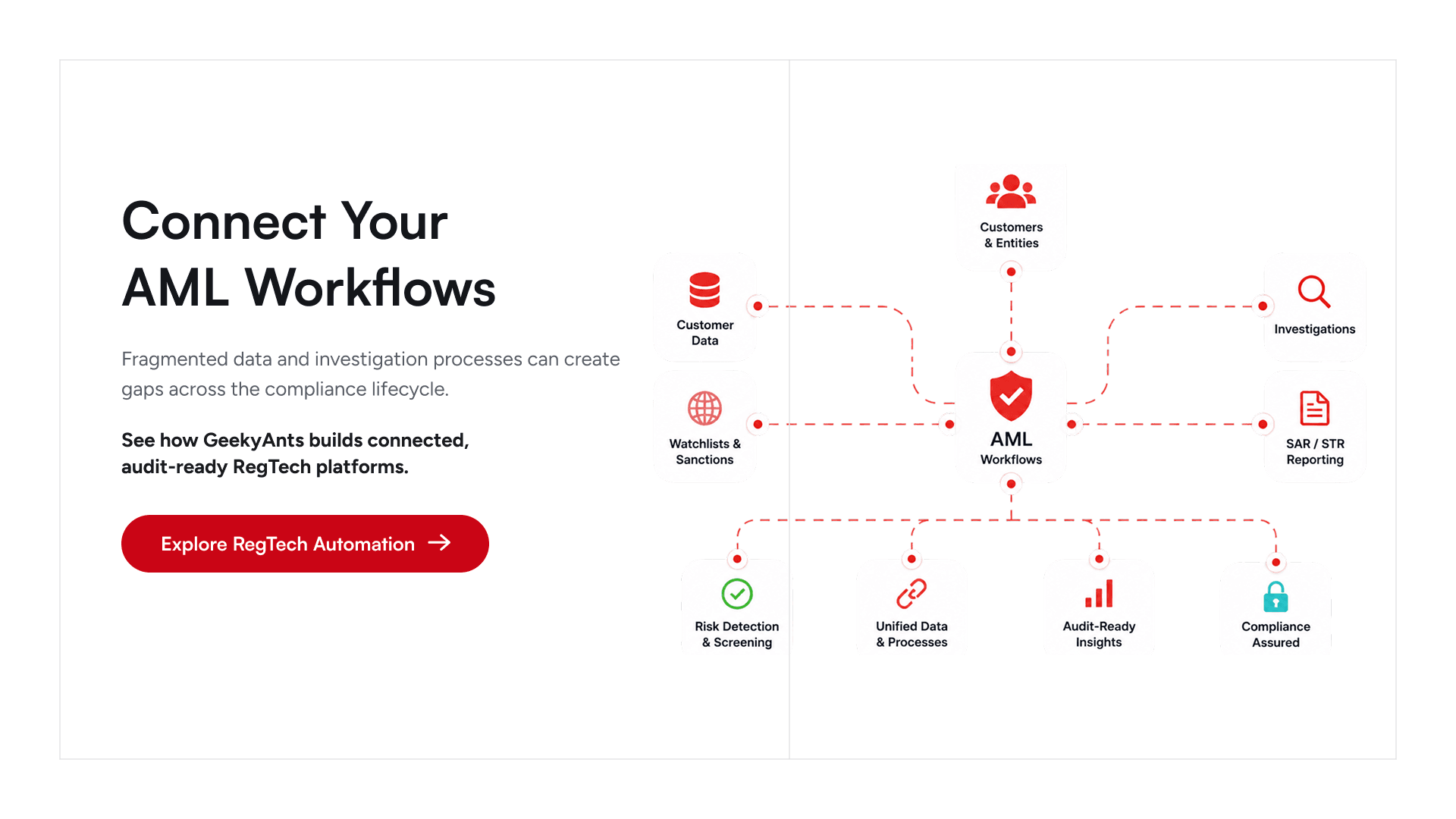

A strong AML setup does not rely on one layer of control—it integrates multiple systems that communicate, escalate, and adapt as risks evolve. Whether you are building from scratch or evaluating vendors, understanding these components is key to designing a solution that is not only compliant but truly resilient.

Breakdown on Why AML Software is Non-negotiable for Modern Businesses

If your product handles money and your AML system cannot adapt, your risk is not theoretical—it is already present. It has become foundational infrastructure for any company handling financial flows at scale, whether that is a digital bank, a cross-border payments app.

Here are five key reasons why the presence of a strong AML software ecosystem is not optional:

1. Regulatory Obligations are Expanding

Financial businesses need to maintain effective AML controls in the customer transaction lifecycle.

- Broader regulatory coverage: AML obligations now apply across banks, fintech platforms, payment providers, lenders, investments firms, remittance businesses and virtual-asset service providers.

- Continuous compliance: Customer risk, sanctions exposure, and transaction behaviour can change after onboarding. Monitoring must continue throughout the relationship with the customers.

- Evidence of compliance: Businesses must be able to show how alerts were generated, investigated, resolved and reported. Reliable records are an essential part of regulatory reviews.

2. Modern Financial Crime Is Fast, Complex, and Global

Criminal networks now exploit real-time digital channels, from peer-to-peer apps to decentralized exchanges. Without real-time, intelligent AML tools, businesses risk unknowingly becoming conduits for fraud, terrorism financing, or sanctions evasion.

- Faster transaction movement: Real-time payments and digital financial services allow funds to move through before manual teams can identify and respond to the risk in time

- Connected activity: Criminal networks use a vast number of methods such as mule accounts, shell entities, shared devices, nested transactions or repeated low-value transfers to hide relationships

- Cross-border complexity: Transactions involve a plethora of parties- customers, counterparties, currencies involving regulations from several different markets making isolated monitoring quite ineffective.

AML systems must therefore evaluate relationships and behavioral patterns rather than relying only on individual transaction thresholds.

3. Operational Overhead from False Positives Is Unsustainable

Many legacy AML systems trigger alerts on 95–98% false positives, overwhelming investigation teams and slowing legitimate customer activity with low-value cases.

- Investigation overload: Analysts end up reviewing repetitive or low-risk alerts instead of credible threats.

- Customer friction: Unnecessary payment hold-ups and repeated verification requests delay transactions and weaken customer experience.

- Higher compliance costs: Businesses need larger and larger investigation teams as alert volumes grow.

Advanced AML software using machine learning, behavioral analytics, and dynamic risk scoring can reduce false positives by 30–50%, helping compliance teams focus on high-risk events without burning out.

4. Trust Depends on Visible and Auditable Controls

AML is no longer back-office hygiene. It is a front-line signal of how seriously a business takes responsibility.

- Regulatory confidence: Clear workflows and audit trails prove that an organization is accountable and consistent.

- Commercial relationships: Banks, payment processors and financial partners prioritize AML maturity over newer products or markets

- Business reputation: The way a business handles its financial risks is directly proportional to customer and investors trust.

Modern businesses—especially those in fintech, crypto, and embedded finance—are expected to prove, not just claim, that their risk and compliance systems are trustworthy, auditable, and aligned with best practices.

5. Legacy Tools Can Restrict Product Growth

AML systems built around fragmented tools, static rules and lengthy manual processes often struggle as their products become more and more complex.

- Limited integration: Legacy systems cannot connect with multiple KYC providers, adjust risk scoring for regional regulations, and scale with product velocity.

- Inflexible controls: Hardcoded rules make it difficult to adjust to varying thresholds, report workflows and risk models

- Scaling challenges: Singular system designs that work for one product or marker does not support newer transaction types, higher volumes and eventually becomes a growth barrier.

Companies today operate in multi-party ecosystems, with APIs powering wallets, loans, remittances, and insurance—often across borders.

The goal is to identify meaningful risks and be able to support defensible decisions while closing compliance gaps.

Key players are already fortifying their AML processes. Here are some examples:

- JPMorgan Chase recently allocated more than $1 billion to modernize its AML and fraud infrastructure, leveraging machine learning and natural language processing to reduce false positives and surface harder-to-catch patterns.

- HSBC has rolled out an AI-driven AML platform that automates the review of millions of alerts with 99%+ accuracy in some segments.

- Deutsche Bank has invested heavily in cloud-based AML systems as part of its broader “transformation” program.

AML Regulations in Different Global Regions

AML requirements vary widely across jurisdictions, not only in terms of reporting thresholds and regulatory bodies, but also in how risk is defined and operationalized. While most countries align with global standards set by FATF, each jurisdiction implements its own interpretation—through local laws, reporting thresholds, and enforcement policies.

Below is a breakdown of the key global frameworks and a comparative view of how regulations differ regionally.

| Jurisdiction | Primary Law/Body | SAR Trigger Threshold | PEP/Watchlist Screening | Real-Time Monitoring Mandated? | Beneficial Ownership Registry |

| United States | BSA / FinCEN | Suspicion-based | Mandatory (OFAC, PEPs) | Not mandatory, but expected | No federal registry (planned) |

| European Union | 6AMLD / Local FIUs | Suspicion-based | Mandatory + EU lists | Expected for fintechs & banks | Required across member states |

| India | PMLA / FIU-IND | INR 10 lakh (~$12K USD) | Mandated by RBI Guidelines | Increasingly expected | In progress (MCA-21 integration) |

| Singapore | MAS AML Guidelines | Suspicion-based | Mandatory + local sanctions | Required for licensees | Required for certain entities |

| Canada | PCMLTFA / FINTRAC | CAD 10,000 | Mandatory (including PEPs) | Recommended for high-risk sectors | Required |

| Australia | AML/CTF Act / AUSTRAC | AUD 10,000 | Mandatory | Required for digital currency | Required |

Each region in the world presents its own set of expectations, reporting protocols, and regulatory pace. If your AML solution is meant to scale across borders, it must be configurable by region, locally compliant by default, and auditable at every layer.

Here are some of the regulatory landscapes worldwide.

1. United States: The Enforcement Powerhouse

The United States has one of the most stringent and enforcement-driven AML frameworks in the world. At its core is the Bank Secrecy Act (BSA), enacted in 1970, which requires financial institutions to assist government agencies in detecting and preventing money laundering. This includes reporting suspicious activity (via Suspicious Activity Reports or SARs), maintaining detailed transaction records, and implementing robust customer due diligence (CDD) processes.

The BSA was significantly strengthened by the USA PATRIOT Act in 2001, which introduced enhanced due diligence for foreign accounts, stricter identity verification standards, and expanded the definition of "financial institutions" to include a broader range of entities such as money service businesses and fintech platforms. The Anti-Money Laundering Act of 2020—part of the National Defense Authorization Act—further modernized AML regulation by mandating beneficial ownership reporting, giving FinCEN expanded authority, and pushing for greater use of technology in AML programs.

U.S. enforcement bodies such as FinCEN, the Office of the Comptroller of the Currency (OCC), and the Department of Justice (DOJ) are aggressive in holding institutions accountable. Penalties can be severe, reaching billions of dollars, and individuals—including compliance officers and executives—can be held personally liable. The U.S. is also strict about real-time monitoring, full transactional visibility, and adherence to sanction screening protocols (especially OFAC lists). Any AML system deployed in the U.S. must be robust, audit-ready, and capable of adapting to complex and evolving regulatory demands.

2. European Union: A Harmonized but Diverse Framework

The EU operates under the 6th Anti-Money Laundering Directive (6AMLD), which mandates risk-based AML programs, centralized beneficial ownership registries, and extended criminal liability for both individuals and corporations. While the directive sets a unified standard, local implementation varies across member states. Germany’s BaFin, France’s ACPR, and Italy’s Bank of Italy have unique enforcement styles and risk definitions. Post-Brexit, the UK operates under its own Money Laundering Regulations (MLRs), enforced by the FCA, though it still aligns with FATF standards. AML software used in Europe must accommodate country-specific rule mapping, multi-language support, and regional risk parameters.

3. India: Compliance Under the Prevention of Money Laundering Act (PMLA)

India enforces its AML framework through the Prevention of Money Laundering Act (PMLA), regulated by the Financial Intelligence Unit – India (FIU-IND). Institutions must follow KYC norms as defined by the RBI, report cash transactions above ₹10 lakh, and file Suspicious Transaction Reports (STRs). The compliance burden is increasing for fintechs, NBFCs, and crypto platforms, especially with new data localization mandates and digital onboarding rules. AML systems deployed in India must support multi-language UIs, threshold-based alerts, and direct integration with FIU-IND reporting APIs.

4. Singapore: Technology-First, Risk-Based Regulation

Singapore’s Monetary Authority of Singapore (MAS) sets AML standards under its Notices 626 and 824, with a strong emphasis on risk-based approaches, digital KYC, and enhanced due diligence for high-risk clients. Virtual asset service providers (VASPs) and fintech companies must comply with sector-specific guidance, including real-time monitoring, blockchain forensics, and continuous screening. The MAS also encourages the use of regtech solutions and AI-powered systems, making Singapore one of the most progressive AML environments in Asia. AML software here must offer configurability, machine learning capabilities, and reporting compliance with STR formats defined by the Commercial Affairs Department (CAD).

5. Canada: FINTRAC and the PCMLTFA

Canada’s AML regime is governed by the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), with oversight from FINTRAC. Institutions are required to verify client identities, report large cash and international electronic transfers, and implement ongoing monitoring. Canada mandates beneficial ownership transparency and sector-specific guidance for casinos, real estate, and MSBs. AML systems in Canada must support CAD-based transaction thresholds, dual-language compliance, and case management tools that align with FINTRAC’s review standards.

6. Australia: Strong Compliance Culture via AUSTRAC

Australia’s AUSTRAC enforces the AML/CTF Act, covering banks, remitters, gaming institutions, and digital currency exchanges. Key requirements include customer identification procedures, reporting of threshold transactions and international transfers, and risk assessments for new technologies. The regulator has shown zero tolerance for non-compliance, issuing heavy fines and license suspensions. AML platforms in Australia must support real-time transaction scanning, Australian PEP/sanctions list integration, and audit trails aligned with AUSTRAC’s guidance.

Each region in the world presents its own set of expectations, reporting protocols, and regulatory pace. If your AML solution is meant to scale across borders, it must be configurable by region, locally compliant by default, and auditable at every layer.

1. United States: The Enforcement Powerhouse

The United States has one of the most stringent and enforcement-driven AML frameworks in the world. At its core is the Bank Secrecy Act (BSA), enacted in 1970, which requires financial institutions to assist government agencies in detecting and preventing money laundering. This includes reporting suspicious activity (via Suspicious Activity Reports or SARs), maintaining detailed transaction records, and implementing robust customer due diligence (CDD) processes.

The BSA was significantly strengthened by the USA PATRIOT Act in 2001, which introduced enhanced due diligence for foreign accounts, stricter identity verification standards, and expanded the definition of "financial institutions" to include a broader range of entities such as money service businesses and fintech platforms. The Anti-Money Laundering Act of 2020—part of the National Defense Authorization Act—further modernised AML regulation by mandating beneficial ownership reporting, giving FinCEN expanded authority, and pushing for greater use of technology in AML programs.

U.S. enforcement bodies such as FinCEN, the Office of the Comptroller of the Currency (OCC), and the Department of Justice (DOJ) are aggressive in holding institutions accountable. Penalties can be severe, reaching billions of dollars, and individuals—including compliance officers and executives—can be held personally liable. The U.S. is also strict about real-time monitoring, full transactional visibility, and adherence to sanction screening protocols (especially OFAC lists). Any AML system deployed in the U.S. must be robust, audit-ready, and capable of adapting to complex and evolving regulatory demands.

2. European Union: A Harmonized but Diverse Framework

The EU operates under the 6th Anti-Money Laundering Directive (6AMLD), which mandates risk-based AML programs, centralized beneficial ownership registries, and extended criminal liability for both individuals and corporations. While the directive sets a unified standard, local implementation varies across member states. Germany’s BaFin, France’s ACPR, and Italy’s Bank of Italy have unique enforcement styles and risk definitions. Post-Brexit, the UK operates under its own Money Laundering Regulations (MLRs), enforced by the FCA, though it still aligns with FATF standards. AML software used in Europe must accommodate country-specific rule mapping, multi-language support, and regional risk parameters.

3. India: Compliance Under the Prevention of Money Laundering Act (PMLA)

India enforces its AML framework through the Prevention of Money Laundering Act (PMLA), regulated by the Financial Intelligence Unit – India (FIU-IND). Institutions must follow KYC norms as defined by the RBI, report cash transactions above ₹10 lakh, and file Suspicious Transaction Reports (STRs). The compliance burden is increasing for fintechs, NBFCs, and crypto platforms, especially with new data localization mandates and digital onboarding rules. AML systems deployed in India must support multi-language UIs, threshold-based alerts, and direct integration with FIU-IND reporting APIs.

4. Singapore: Technology-First, Risk-Based Regulation

Singapore’s Monetary Authority of Singapore (MAS) sets AML standards under its Notices 626 and 824, with a strong emphasis on risk-based approaches, digital KYC, and enhanced due diligence for high-risk clients. Virtual asset service providers (VASPs) and fintech companies must comply with sector-specific guidance, including real-time monitoring, blockchain forensics, and continuous screening. The MAS also encourages the use of regtech solutions and AI-powered systems, making Singapore one of the most progressive AML environments in Asia. AML software here must offer configurability, machine learning capabilities, and reporting compliance with STR formats defined by the Commercial Affairs Department (CAD).

5. Canada: FINTRAC and the PCMLTFA

Canada’s AML regime is governed by the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), with oversight from FINTRAC. Institutions are required to verify client identities, report large cash and international electronic transfers, and implement ongoing monitoring. Canada mandates beneficial ownership transparency and sector-specific guidance for casinos, real estate, and MSBs. AML systems in Canada must support CAD-based transaction thresholds, dual-language compliance, and case management tools that align with FINTRAC’s review standards.

6. Australia: Strong Compliance Culture via AUSTRAC

Australia’s AUSTRAC enforces the AML/CTF Act, covering banks, remitters, gaming institutions, and digital currency exchanges. Key requirements include customer identification procedures, reporting of threshold transactions and international transfers, and risk assessments for new technologies. The regulator has shown zero tolerance for non-compliance, issuing heavy fines and licence suspensions. AML platforms in Australia must support real-time transaction scanning, Australian PEP/sanctions list integration, and audit trails aligned with AUSTRAC’s guidance.

These differences mean that a one-size-fits-all compliance strategy will quickly fail.

Must-Have Features in AML Software

If you are building or integrating AML infrastructure into your product, these are the core features you need to get right. They are not feature requests—they are foundational requirements that determine whether your AML system can operate under pressure, scale with your product, and satisfy global regulators.

1. Real-Time Transaction Monitoring

Definition: The ability to detect suspicious transactions as they happen, not after the fact.

You need an event-driven architecture that processes transactions in milliseconds. If detection happens after the funds move, it is already too late. For modern fintechs and cross-border platforms, real-time monitoring is the difference between prevention and postmortem.

2. Customizable Rules Engine

Definition: A logic layer where compliance teams can define and update risk detection rules.

You will not catch edge-case risks with out-of-the-box vendor rules. You need a system where business users—not just engineers—can create, modify, and prioritize rules with minimal friction. Bonus if the rule engine supports versioning, testing, and dynamic parameters.

3. Dynamic Risk Scoring

Definition: A system that assigns and updates a risk score for users, transactions, or accounts based on evolving behavior.

A user’s risk level should not be fixed at onboarding. If their velocity spikes, or if they interact with new geographies or entities, the score should reflect that immediately. The system must continuously calculate and adjust based on internal and external signals.

4. Multi-Jurisdictional Compliance Mapping

Definition: The ability to tailor compliance behavior based on regional laws and regulatory thresholds.

Different countries have different SAR thresholds, reporting formats, and retention periods. You need an AML system that supports localized logic without having to fork code every time you enter a new market. Look for region-aware rulesets and templated reporting outputs.

5. PEP and Sanctions Screening with API Support

Definition: The process of matching users and counterparties against politically exposed persons (PEPs) and global sanctions lists via API.

You must screen against OFAC, EU, UN, and other jurisdiction-specific lists—and do so continuously. The system should support onboarding-time screening and live transaction-time screening, ideally with enrichment via third-party APIs for updated risk context.

6. Alert Management and Case Resolution Workflow

Definition: A structured process for investigating, escalating, and resolving flagged events.

Once an alert is generated, you need an internal system for triaging, assigning, commenting, and closing the case. Investigators should be able to link related alerts, set SLA timers, attach notes, and build an audit-ready timeline. Think like a CRM for risk resolution.

7. Automated Regulatory Reporting

Definition: A mechanism that generates and formats required reports (e.g., SARs, STRs, CTRs) for submission to financial intelligence units (FIUs).

These reports are mandatory in most jurisdictions and must be precise. Your system should pre-fill forms, validate completeness, and allow final review before submission. Ideally, it supports regulator-specific export formats (e.g., XML, JSON, PDF).

8. Audit Logs and Forensic Visibility

Definition: Immutable records of every action taken, rule triggered, decision made, and report submitted within the AML system.

When auditors or regulators show up, you need proof—logs that show who did what, when, and why. Every alert, override, comment, and rule change must be recorded in a tamper-evident way. Forensic visibility is your legal defense.

9. Scalable Data Infrastructure

Definition: Backend architecture that can handle high-volume, high-frequency data across multiple sources.

You are not building a dashboard—you are building a streaming data system. Your AML layer must support time-series event joins, real-time aggregation, historical lookbacks, and long-term archiving. If you plan to scale users, this is non-negotiable.

10. Fallback and Fail-Safe Mechanisms

Definition: Built-in controls that activate when the AML system goes down or fails to respond in time.

No system is 100% reliable. If screening is delayed or unavailable, what happens to the transaction? You need policy-driven controls that block, queue, or escalate the event. Silent failures are not acceptable when compliance is on the line.

If you leave any of these pieces out, you are not building AML—you are outsourcing risk and hoping for the best. A robust AML system is not just about catching bad actors. It is about proving that you have built the infrastructure to catch them before the regulators come asking.

“If your AML system cannot monitor transactions in real time, generate auditable alerts, and adapt rules per region, then it is not a compliance system—it is a liability. Every core component, from dynamic risk scoring to automated regulatory reporting, must be built with scale, speed, and scrutiny in mind.”

- Kunal Kumar, CRO, GeekyAnts

AML Software Development Process - Building A Strong Firewall to Illegal Transactions

If you are building an AML application, you are not just adding a compliance feature—you are designing a critical layer of your product’s security and credibility. AML software needs to act like a firewall: always on, always watching, and ready to flag what humans miss. It must be fast, audit-ready, regionally aware, and impossible to ignore when it matters.

Here is how you should approach it—with the right architecture, teams, and partners.

1. Start with Regulatory Mapping and Risk Exposure

Before you touch code, understand what regulations apply to your product. If you operate in the U.S., you need to align with the Bank Secrecy Act (BSA) and FinCEN guidelines. In the EU, it is 6AMLD. In India, it is PMLA. Singapore? MAS AML notices. Do not generalize. Map your operational footprint to the specific laws in those regions and define your risk surface—what kinds of users, transactions, and geographies you are exposed to. You cannot build effective controls without knowing what you are controlling for.

Who you will need:

- Legal or compliance lead

- Risk analyst

- External AML advisor (especially for international operations)

Key considerations include:

- jurisdictions and regulatory authorities

- customer and business types

- transaction methods, currencies, and geographic corridors

- KYC, screening, monitoring, and reporting obligations

- data-retention and privacy requirements

- high-risk products, users, or transaction patterns

This stage should result in a compliance requirements matrix and a defined risk model that guide the rest of the build.

You should treat each AML function as a microservice: transaction monitoring, sanctions screening, KYC/CDD, risk scoring, alerting, and reporting. Keep them loosely coupled but well integrated. Use event streams (like Kafka or Pub/Sub) to trigger risk evaluations and avoid blocking the core product experience.

Suggested Tech Stack:

- Backend: Node.js, Python, or Go (for concurrency-heavy workloads)

- Databases: PostgreSQL (case data), Redis (risk state), MongoDB (KYC metadata)

- Streaming: Apache Kafka or Google Pub/Sub

- Infrastructure: Kubernetes, Docker, Prometheus, Grafana, Vault

- Frontend: React.js with Tailwind (for internal tools)

How Can GeekyAnts Help:

If your team is lean, backend-heavy, or already focused on core product delivery, that is where we come in. At GeekyAnts, we help you move faster by taking ownership of the parts that need to be built right the first time—internal compliance dashboards, case management systems, frontend interfaces, and scalable APIs that plug seamlessly into your AML stack.

We bring the design, engineering, and delivery muscle to help you ship faster, without adding overhead to your team. You focus on your core risk logic—we’ll take care of the tools that support it.

3. Build a Customizable Rules Engine and Risk Layer

Do not hardcode detection logic. Your compliance team needs control. Build a rule engine where they can define thresholds (e.g., 5 transfers over $10,000 in 24 hours), flag behaviors (e.g., velocity changes, geolocation mismatches), and experiment with logic without engineering help. Tie that to a real-time risk scoring system that updates dynamically as behavior shifts.

Who you will need:

- Backend engineer (rules engine)

- Data engineer or ML engineer (for future anomaly detection)

- Compliance analyst (embedded in the build phase)

Tooling Tip:

Start with rules—then later layer in machine learning to reduce false positives and surface patterns your rules missed. Keep the models explainable or your auditors will push back.

4. Build Alerting, Case Management, and Reporting Tools

When something triggers an alert, your system should know what to do. Queue the alert, route it to a reviewer, allow comments, escalation, case linking, and auto-generate reports like SARs, STRs, or CTRs. Track every action. You will need this audit trail when the regulator asks for it—because eventually, they will.

Who you will need:

- Backend + frontend engineers

- Product manager (compliance tools)

- QA team (workflow testing)

Bring in GeekyAnts here if needed:

If you need a custom, lightweight internal tool for your compliance team, we can build it faster and cleaner than an overstretched internal squad. Our design-to-code approach allows us to quickly deliver polished, functional interfaces—whether it's modals, dashboards, filters, or audit views. We focus on speed, usability, and seamless integration, so your team gets exactly what they need without slowing down your core development.

5. Prepare for Continuous Adaptation

Your system cannot be static. Watchlists update. Thresholds shift. Risk typologies evolve. You should allow your team to update rules, ingest new PEP/sanctions lists, and flag new threat patterns without rolling a new build. Build with change in mind.

Optional Advanced Layer:

- Integrate anomaly detection models

- Run unsupervised learning on transaction patterns

- Use alert feedback loops to improve triage accuracy over time

You will need:

- A DevOps pipeline for compliance config

- Version control for rule changes

- Data observability to detect drift or gaps

Partnering Smart Makes Your Go-to-Market Faster

You do not need to build everything in-house to maintain control. The smart move is to own the core risk logic while outsourcing non-differentiating components like dashboards, case tools, or integrations to engineering partners who can move fast without compromising quality. GeekyAnts fits this role well—we understand compliance-driven workflows and can ship polished, scalable interfaces that slot into your backend without friction.

How Emerging Technologies Are Transforming AML Software

AML software is undergoing a major shift—from static, rules-based systems to intelligent, adaptive platforms that learn, evolve, and act faster than ever before. This transformation is not just a technological upgrade—it is a response to the scale and speed of modern financial crime. Traditional systems, built around fixed thresholds and manual reviews, are no longer enough. The complexity of today's transactions—driven by real-time payments, crypto rails, embedded finance, and cross-border flows—requires smarter systems that can understand context, predict intent, and reduce noise without missing risk.

At the center of this shift is artificial intelligence, particularly machine learning (ML). AI is redefining how AML software detects suspicious activity. Instead of relying solely on pre-set rules (e.g., “flag anything over $10,000”), modern systems now use both supervised and unsupervised models to detect anomalies, cluster behaviors, and identify previously unseen typologies. These models learn from historical case data—flagged transactions, confirmed false positives, investigator feedback—and adjust continuously. The result: fewer false positives, faster escalations, and better detection of hidden risk.

How AI is actively transforming core AML components

- Anomaly Detection – ML models flag deviations from normal behavior, even if no explicit rule exists. Useful for spotting mule accounts, circular fund flows, or hidden structuring.

- Risk Scoring Optimization – AI adjusts user or transaction risk scores dynamically, based on behavioral patterns, device intelligence, and past interactions.

- Alert Prioritization – Instead of dumping all alerts on analysts, systems rank and route them based on contextual risk—saving hours per case.

- False Positive Reduction – Pattern recognition helps identify which alerts are consistently benign, cutting alert volume by 30–50% in mature systems.

- Natural Language Analysis – NLP models can extract intent or context from KYC documents, unstructured notes, or chat logs—useful in SAR creation and fraud communication detection.

Recent developments show how fast this space is evolving. In 2024, HSBC reported a 38% reduction in false positives after rolling out AI-driven alert triage. J.P. Morgan developed an in-house AI platform to monitor high-frequency trades and transaction layering in real time. Startups like Hawk AI and ComplyAdvantage are offering real-time AML APIs that integrate explainable AI (XAI), allowing compliance officers to view the logic behind every alert—critical for both internal trust and regulatory acceptance.

Looking ahead, the future of AML software will be autonomous, explainable, and globally contextual. Systems will not just raise alerts—they will make real-time decisions, auto-freeze funds when thresholds are crossed, and dynamically adapt to new laundering typologies. AML tools will integrate with behavioral analytics, biometrics, blockchain forensics, and voice/text intelligence to assess intent, not just activity. And crucially, they will be auditable by design—with traceable decision logs and algorithmic transparency to meet growing regulatory demands.

For any company building AML capabilities today, the direction is clear. Emerging technologies are not just enhancements—they are prerequisites for surviving and scaling in an environment where compliance, speed, and intelligence must coexist by default. If your AML stack cannot learn, adapt, and explain itself, it is already behind.

Real-World Case Studies of AML Law Violations

Understanding how major institutions failed to meet AML obligations offers sharp lessons for any business building financial infrastructure today. These are not abstract headlines—they are blueprints for what to avoid. Below are brief but powerful examples of real-world AML violations, what caused them, and what modern companies should learn from them.

1. Danske Bank (Estonia Branch, €200 Billion Laundering Scandal)

What happened: Between 2007 and 2015, Danske Bank’s Estonian branch processed over €200 billion in suspicious, non-resident transactions. Most of the funds originated from Russia, Azerbaijan, and Moldova, routed through shell companies.

Why it happened: The bank lacked proper transaction monitoring systems in its Baltic branches. Senior management failed to act on internal warnings, and compliance was structurally siloed and underfunded.

Key learning: Do not treat compliance as a regional issue. AML systems and controls must operate consistently across branches, subsidiaries, and third-party integrations.

2. Westpac (Australia, AUSTRAC Fine of AUD 1.3 Billion)

What happened: In 2020, Westpac was fined AUD 1.3 billion by Australia’s AML regulator for 23 million breaches, including failure to report international funds transfers and links to child exploitation payments.

Why it happened: Legacy systems did not capture certain transaction types, and reporting processes were fragmented. There was poor integration between risk, product, and compliance teams.

Key learning: You must build AML infrastructure that works across all transaction types—including small-value, cross-border, and niche product flows. "Too minor to monitor" is no longer acceptable.

3. TD Bank (U.S., $3 Billion Penalty in 2024)

What happened: TD Bank allowed over $670 million in drug cartel-related funds to flow through its U.S. operations, and 92% of its transaction volume went unscreened. Five bank employees were directly involved in facilitating illicit transfers.

Why it happened: The bank failed to upgrade its AML systems, excluded entire categories of transactions from screening, and prioritized customer experience over compliance.

Key learning: If your AML system does not monitor 100% of transaction volume in real time, you are operating blind. Gaps in coverage can—and will—be exploited.

4. ING (Netherlands, €775 Million Fine in 2018)

What happened: ING was fined €775 million for failing to prevent money laundering over a six-year period. Criminals used ING accounts to launder millions via fake invoices and straw companies.

Why it happened: ING did not apply sufficient due diligence, failed to identify beneficial owners, and ignored clear signs of high-risk behavior.

Key learning: AML is not just about monitoring transactions—it is also about onboarding and continuous customer due diligence. Skipping identity or ownership checks undermines the entire risk model.Why Top FinTechs Trust GeekyAnts for AML Software

Modern AML systems demand more than just feature development—they require a product engineering partner who understands how financial infrastructure operates at scale, under regulatory pressure, and in real-time market conditions. At GeekyAnts, we do not just write code. We co-create scalable compliance systems that evolve from product strategy to market readiness, and then into growth-focused engines that sustain trust across jurisdictions.

Our experience in fintech is deep and deliberate. We have worked with global payments networks, public sector banks, neobanks, BNPL platforms, and crypto-first startups—helping them ship products that move money securely, reduce risk exposure, and pass scrutiny from regulators and auditors alike. But what sets us apart is not just our technical execution—it is our understanding of the product lifecycle in regulated spaces.

From your first MVP build (with rapid prototyping of KYC/CDD flows or sanctions API integration) to feature refinement and alert automation, we help you stand up robust AML features quickly, without compromising long-term scale. As your user base grows and regulatory oversight deepens, we help you modularize AML systems, implement AI-driven transaction analysis, and design internal dashboards that make compliance teams more productive—not buried in noise.

This thinking is embedded in our fintech development framework:

- Product Strategy: AML use-case modeling, jurisdictional compliance scoping, and rules engine design.

- Product Engineering: Modular microservices for risk scoring, fraud detection, PEP/OFAC screening, and KYC orchestration.

- Product Growth: Case management interfaces, anomaly detection models, SAR/STR reporting automation, and alert optimization via feedback loops.

This is the same playbook that has helped our partners process over 1.2 million global transactions per month, integrate with 20+ payment and compliance vendors, and go live across multi-jurisdictional markets—with audit logs, risk profiles, and user trust intact.

Backed by our dedicated FinTech division and an R&D team exploring emerging regtech trends, we also stay ahead of the curve with innovations in:

- Embedded AML for embedded finance platforms

- Real-time fraud flagging integrated into consumer UIs

- Machine learning for transaction pattern scoring

- AML tooling tailored for crypto compliance and NFT finance

Our goal is simple: help you build an AML foundation that is as scalable as your product ambition. Because if trust is your brand currency, compliance is the ledger it lives on.

Case Study 1: Building a Global Payments Platform Handling 1.2M+ Transactions

FinTech Mobile & Web App for Global Payment Processing

We partnered with a global payments firm to build an end-to-end web and mobile application that supports 1.2 million+ monthly transactions across 20+ currencies and 50+ countries. The product required seamless integration with third-party KYC providers, real-time fraud flagging, and multi-level approval workflows—all essential building blocks of a robust AML ecosystem.

Key Contributions:

- Built dynamic, region-aware transaction modules for high-risk corridor screening.

- Designed multi-currency reconciliation and compliance-ready logs.

- Created a scalable architecture that could plug in AML APIs (for PEP/sanctions, velocity checks, etc.) without architectural rework.

This solution is a real-world AML-adjacent system—where laundering risk, transaction orchestration, and audit trails had to coexist in a single experience.

Case Study 2: AI-Powered AML Insight Layer for Indian Public Sector Bank

AI-Powered Mobile App Upgrade for a Major Indian Bank

Working with one of India’s leading public sector banks, we modernized their mobile banking platform while adding an AI-based transaction pattern monitoring system that could flag potential anomalies in user behavior. With a user base exceeding 2 million and transaction volumes crossing ₹500 crore/month, precision was critical.

Key Contributions:

- Integrated behavior-based machine learning for risk scoring and abnormal activity detection.

- Designed audit-ready user journeys with event-level logging for compliance review.

- Created real-time visualizations for transaction flows and KYC failure patterns—empowering internal compliance teams.

The result was a compliance-grade mobile experience ready for integration with PMLA reporting requirements and future FATF audit trails.

Conclusion

Building a future-ready AML system is no longer a regulatory checkbox—it is a strategic imperative. The challenges are real: growing transaction complexity, fragmented global laws, rising enforcement pressure, and the constant evolution of criminal tactics. But the opportunity is just as real. With the right architecture, intelligent automation, and jurisdiction-aware design, AML software becomes more than a defense mechanism—it becomes a competitive advantage.

For businesses operating in today’s financial ecosystem, the message is clear: invest early, build smart, and stay adaptive. AML systems built today must be ready for what compliance, fraud, and global scale will look like tomorrow.

FAQs about AML Software Development

Subscribe to Our Newsletter

Subscribe to RSS

Press & Media Hub RSS FeedRelated Articles.

More from the engineering frontline.

Dive deep into our research and insights on design, development, and the impact of various trends to businesses.

Aug 4, 2026

Building AI-Powered Banking CRM Platforms Without Replacing Core Banking Systems

Jul 20, 2026

AI Operators in Insurance: Improving Customer Experience Through Intelligent Automation

May 22, 2026

AI in Insurance: Building Production-Ready Products for Claims, Underwriting, and Customer Experience

May 22, 2026

Building AI Investment Platforms: From Predictive Analytics to Personalized Portfolio Insights

May 21, 2026

Explainable AI in Insurance Underwriting: Balancing Accuracy and Compliance

Jan 27, 2026